Ron Stasch, a mentor to our founders and an early leader in the 1031 exchange industry, approached real estate with a level of discipline and clarity that remains highly relevant. His perspective was not built on theory alone, but on decades of advising investors through changing markets, cycles, and objectives.

“Most real estate investors don’t fail because they the choose the wrong property.

They fall short because they choose the wrong strategy for where they are.”

Trading vs. Investing and 1031 Exchange Strategy

One of the most important distinctions Ron Stasch made was that there are two main theories for wealth-building in real estate: trading and investing.

- A “trader” is someone who buys real estate and sells when it matures or “peaks”.

- An “investor” is someone who buys real estate and holds it for a very long time… sometimes forever. We also refer to this kind of investor as being a “holder”.

Real estate is such a complex area of investment that either of these methods will create wealth. It is the rate of wealth-building that differs.

For Ron Stasch, the 1031 Exchange was more than a tax-deferral tool. It was a strategic mechanism that allowed investors to reposition capital, pursue larger opportunities, and accelerate wealth creation without unnecessarily reducing equity through taxation.

A Tale of Two Investors

A young couple borrowed $6,000 to purchase a triplex in 1970 for $70,000. Fifteen years later, they sold it for $270,000, achieving an annual return of approximately 29%.

During that same period, another investor began with $14,000 and actively repositioned into larger opportunities as they emerged. By 1986, that investor controlled over $10,000,000 in property and $4,000,000 in equity.

The Difference Wasn’t the Market – It Was the Approach

While the triplex owners benefited from steady income, the active investor accepted short-term instability in exchange for long-term growth. Today, that investor has transitioned into holding and enjoys substantial passive income, while the triplex owners will likely depend on traditional retirement income.

It is, of course, possible to combine both approaches. Many investors acquire property and hold it long enough to access additional capital through refinancing, using that capital to expand their portfolio. While this can provide a sense of stability, it also introduces limitations.

Growth becomes dependent on market cycles and lending conditions, and smaller properties may only generate enough equity to acquire similarly sized assets. At some point, consolidation or repositioning may still be necessary to create meaningful income.

Knowing When to Trade and When to Hold

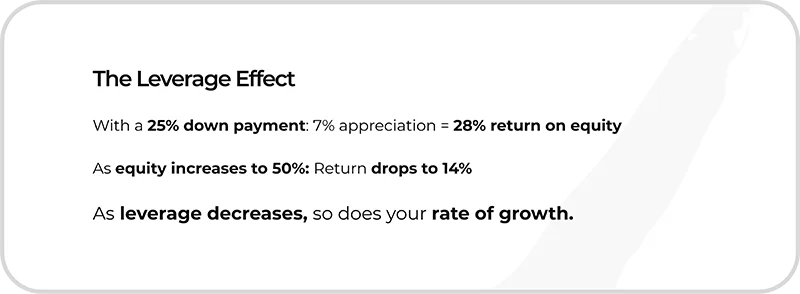

In deciding whether to trade or hold, it is important to view your property as though you were acquiring it with your equity as a down payment. If you own a 20-unit complex valued at $1,200,000 and you have net equity (after sales costs and taxes) of $500,000, ask yourself, “Would I buy this building for $1,200,000 with a $500,000 down payment?”

If you are trying to build wealth, the answer is usually, “No”. If the cash flow is $35,000 per year and you are at the end of your investment plan, you may very well decide that the cash flow (7% on net equity) justifies such a purchase. If you keep this property, you have, in effect, purchased it under these conditions.

Traders grow more rapidly than holders if they pay attention to their properties and to the market. If a recession is on the way, traders should do very well, holders will suffer. Once the level of equity is reached that will provide a desirable cash flow, holding becomes the most effective wealth-building technique.

The ideas Ron Stasch shared decades ago remain just as relevant today.

His belief that strategy matters more than any single property continues to shape how investors approach real estate and the 1031 Exchange. By understanding when to trade, when to hold, and how to reposition capital effectively, investors can make decisions that support long-term wealth creation.

That philosophy remains at the heart of the 1031 Exchange strategy and is one of the many lessons preserved through The Heritage Series. This article is the first in a series exploring the foundational ideas, principles, and strategies that continue to influence how we approach the 1031 Exchange today.

Key Takeaways

- Trading focuses on repositioning assets to accelerate equity growth.

- Investing focuses on long-term ownership and cash flow.

- A 1031 Exchange allows investors to defer capital gains taxes while repositioning into new opportunities.

- The best strategy depends on an investor’s stage of wealth building.

- Ron Stasch believed that strategy selection is often more important than property selection.

1031 Exchange Strategy FAQs

What is the difference between trading and investing in real estate?

According to Ron Stasch, a trader actively buys and sells investment properties as they mature or reach their highest potential value, using equity to pursue larger opportunities and accelerate wealth growth. An investor, or holder, acquires real estate with the intention of owning it for the long term, relying on appreciation and cash flow to build wealth. Both approaches can be successful. The key difference is the rate of wealth-building and whether an investor is focused on growth or long-term income.

How can a 1031 Exchange support wealth building?

A 1031 Exchange allows investors to defer capital gains taxes when exchanging one investment property for another qualifying property. By preserving equity that would otherwise be lost to taxes, investors can reposition into larger or more productive properties, increase cash flow potential, and continue building wealth over time. Ron Stasch viewed the 1031 Exchange as a strategic tool that helps investors move toward their long-term financial goals.

When should an investor stop trading and begin holding property?

Ron Stasch believed that trading is often the most effective strategy while an investor is focused on building wealth. Once an investor has accumulated enough equity to generate the desired level of passive income, holding property may become the better strategy. At that stage, consistent cash flow and long-term stability often outweigh the benefits of continued repositioning.

Does a 1031 Exchange work for both traders and long-term investors?

Yes. A 1031 Exchange can benefit investors at different stages of their investment journey. Active traders can use exchanges to reposition into larger or better-performing properties while preserving equity. Long-term investors can also use a 1031 Exchange to improve cash flow, consolidate assets, diversify holdings, or acquire properties that better align with their long-term investment objectives.

About Ron Stasch

Ronald C. Stasch, CCIM, NAC, was an early leader in the 1031 Exchange industry whose decades of experience helped shape the thinking of many exchange professionals, including the founders of Equity Advantage Incorporated, a national exchange facilitation company. His practical approach to real estate investing and exchange strategy continues to influence investors today through The Heritage Series.

The Guys With All The Answers…

David and Thomas Moore, the co-founders of Equity Advantage & IRA Advantage

David and Thomas Moore, the co-founders of Equity Advantage & IRA Advantage

Whether working through a 1031 Exchange with Equity Advantage, acquiring real estate with an IRA through IRA Advantage or listing investment property through our Post 1031 property listing site, we are here to help Investors get where they want to be. Call them today! 503-635-1031.