State Mandatory Withholding

Most states impose a state income tax when real estate is sold. To ensure that the state collects this income tax from a non-resident seller, some states collect the tax at closing. This type of collection is called a state mandatory withholding.

Each state varies on how it collects the tax withholding. The state may place the burden of collecting the tax withholding upon the buyer. Other states may place the burden on the authorized agent that provides closing and settlement services. The authorized agent may be an attorney, the title officer or an escrow agent (again, the state determines who provides the closing and settlement services.)

The amount of money that the state collects is usually an amount equal to the state income tax. It varies from state to state. It may be a straight percentage of the sales price or it may be a percentage of the net proceeds. The authorized agent who collects the tax withholding may serve as an excellent resource for providing the percentage amount that the state is collecting at closing.

Exemptions

The state may allow an exemption to the mandatory withholding. Usually, the exemption includes property transferred in a 1031 Exchange. To claim the exemption, the non-resident will need to sign an exemption form (or certificate) provided by the state. A state may require the seller to submit the exemption 20 days before closing while other states may allow the exemption form to be submitted at closing. Again, each state has its own specific requirements for claiming the exemption so it is best to consult with the closing/settlement agent or the state website for revenue collection.

Individual States

When people call us about starting a 1031 Exchange, we are frequently asked questions about how state taxes affects a 1031 Exchange. Questions range from marital status to withholding exemptions and how they affect taxpayers selling property using 1031. Below are some helpful articles with basic information and list of links to State’s Tax Board websites. Please be sure to reference information on the State’s website to learn of any information updates.

State-to-State 1031 Exchange Rules on Capital Gains Taxes Investors Should Know

Many real estate investors are unsure if they can use a 1031 Exchange when selling property in one state and purchasing another in a different state. Fortunately, for all the investors out there, moving markets is not an issue when it comes to 1031 Exchanges.

Withholding Requirements

*Some may have withholding exemptions for taxpayers selling property using 1031.

- AL

- CA

- CO

- DE

- GA

- HI

- MD

- ME

- MS

- NC

- NJ

- NY

- OR

- RI

- SC

- VT

- WV

Claw-Back Provisions

- CA

- MA

- MT

- OR

Does Not Follow 1031

- PA- (Consult a tax professional for details)

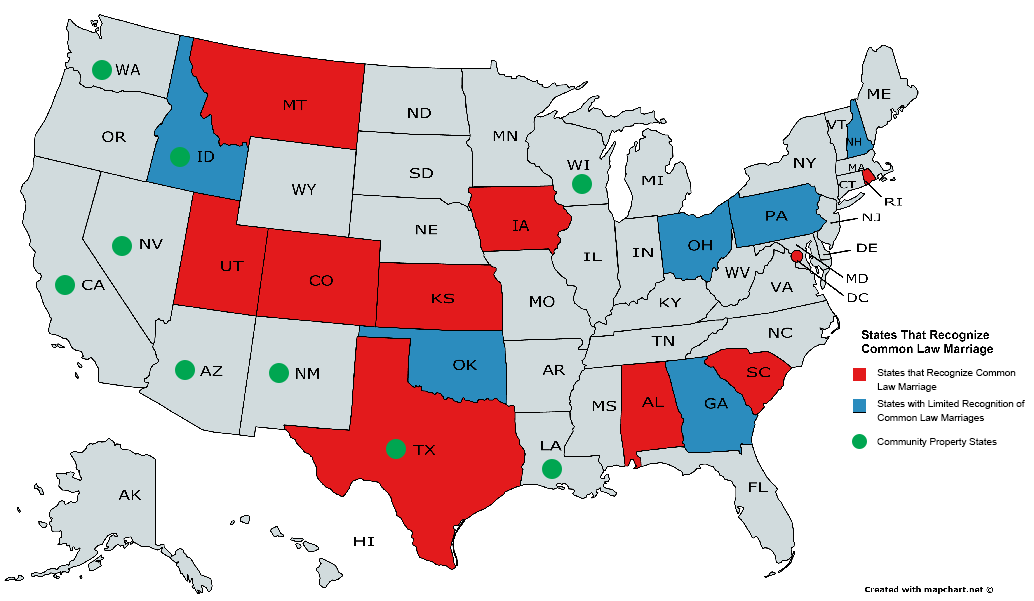

Community Property States vs. Common Law

In community property states, the assets of each spouse are considered assets of the marital unit. The assets of each partner in the relationship are not legally separate from those of the spouse. That is, while a couple is married, creditors of one spouse, with certain restrictions, can seize the assets of both spouses. Map: Red = States that Recognize Common Law Marriage Blue = State with Limited Recognition of Common Law Marriages Green = Community Property States

Community Property States vs. Common Law

- AZ

- CA

- ID

- LA

- NM

- NV

- TX

- WA

- WI

- AK (Depends)

State Individual Income Tax Rates and Brackets for 2020

Individual income taxes are a major source of state government revenue, accounting for 37 percent of state tax collections in fiscal year (FY) 2017. Forty-three states levy individual income taxes. Forty-one tax wage and salary income, while two states-New Hampshire and Tennessee-exclusively tax dividend and interest income.

This information is intended to provide a starting point to determine the website for the state collection department, the withholding amount, and the exemption form. For the most current information, please refer to the particular state’s Tax Board website and (as a suggestion) search for “nonresident withholding tax exemption.”

Select Your State

Alabama

Alabama Department of Revenue

Requirements – N/A

Alaska

Alaska Department of Revenue

Requirements – N/A

Arizona

Arizona Department of Revenue

Requirements – N/A

Arkansas

Arkansas Department of Finance and Administration

Requirements – N/A

California

California Franchise Tax Board

Requirements – 3.3% & Form 593C Pub 1016

Colorado

Colorado Department of Revenue

Requirements – 2% & Form 1083

Connecticut

Connecticut Department of Revenue Services

Requirements – N/A

Delaware

Delaware Division of Revenue

Requirements – N/A

Florida

Florida Department of Revenue

Requirements – N/A

Georgia

Georgia Department of Revenue

Requirements – 3% & Form IT-AFF

Hawaii

Hawaii Department of Taxation

Requirements – 5% & Form N 289

Idaho

Idaho State Tax Commission

Requirements – N/A

Illinois

Illinois Department of Revenue

Requirements – N/A

Indiana

Indiana Department of Revenue

Requirements – 1031 is not recognized unless true swap with simultaneous Exchange. Full Indiana state tax withheld

Iowa

Iowa Department of Revenue and Finance

Requirements – N/A

Kansas

Kansas Department of Revenue

Requirements – N/A

Kentucky

Kentucky Revenue Cabinet–Online Taxpayer Service Center

Requirements – N/A

Louisiana

Louisiana Department of Revenue

Requirements – N/A

Maine

Maine Revenue Services

Requirements – 2.5% & REW-5

Maryland

Maryland Revenue Services

Requirements – 4.75% & Form MW506AE

Massachusetts

Massachusetts

Requirements – N/A

Michigan

Michigan Department of Treasury

Requirements – N/A

Minnesota

Minnesota Department of Revenue

Requirements – N/A

Mississippi

Mississippi Tax Commission

Requirements – Over $100,000 required 5% withholding or net amount realized by seller, whichever is less.

Missouri

Missouri Department of Revenue

Requirements – N/A

Montana

Montana Department of Revenue

Requirements – N/A

Nebraska

Nebraska

Requirements – N/A

Nevada

Nevada Department of Taxation

Requirements – N/A

New Hampshire

New Hampshire Department of Revenue Administration

Requirements – N/A

New Jersey

New Jersey Division of Taxation

Requirements – 8.97% of tax gain on house sold but collection shall not be less than 2% of the consideration & Form GIT/REP-1,4.

New Mexico

New Mexico Taxation and Revenue

Requirements – N/A

New York

New York Department of Taxation & Finance

Requirements – Estimated Tax amount by owner & form IT-2663.

North Carolina

North Carolina Department of Revenue

Requirements – Completion of Form NC-1099NRS but no tax if performing a 1031 tax deferred Exchange.

North Dakota

North Dakota State Tax Department

Requirements – N/A

Ohio

Ohio Department of Taxation

Requirements – N/A

Oklahoma

Oklahoma Tax Commission

Requirements – N/A

Oregon

Oregon Department of Revenue

Requirements – 4% to 10% effective Jan. 1, 2008

Pennsylvania Department of Revenue

Pennsylvania

Requirements – N/A

Rhode Island

Rhode Island Division of Taxation

Requirements – 6% of sales price or total gain for individuals, estates, partnerships or trusts and 9% for nonresident corporations unless the nonresident seller makes gain election and files RI form 71.3.

South Carolina

South Carolina Department of Revenue

Requirements – 5% for corporations, 7% for individuals. Exemption through Form I-295.

South Dakota

South Dakota

Requirements – N/A

Tennessee

Tennessee

Requirements – N/A

Texas

Window on State Government–Texas Taxes

Requirements – N/A

Utah

Utah State Tax Commission

Requirements – N/A

Vermont

Vermont Department of Taxes

Requirements – 2.5% Form RW-171

Virginia

Virginia Department of Taxation

Requirements – N/A

Washington

Washington Department of Revenue

Requirements – 1.7% excise tax upon sale.

Washington D.C.

Washington D.C. Office of Tax and Revenue

Requirements – N/A

West Virginia

West Virginia Department of Revenue

Requirements – N/A

Wisconsin

Wisconsin Department of Revenue

Requirements – N/A

Wyoming

Wyoming Department of Revenue

Requirements – N/A