The Napkin Test was conceived literally on a napkin at a seminar by California tax attorney Marvin Starr of Miller, Starr and Regalia. It’s a simple exercise to determine the potential for exposing taxable assets or “boot” in an Exchange. The Napkin Test compares the values of the relinquished and replacement properties. Although it doesn’t replace a detailed Exchange recapitulation worksheet, the Napkin Test can quickly and easily assess an Exchange and any potential for boot. An Exchange’s ultimate benefit must be established with further assistance from qualified tax or legal counsel.

Here’s The Test

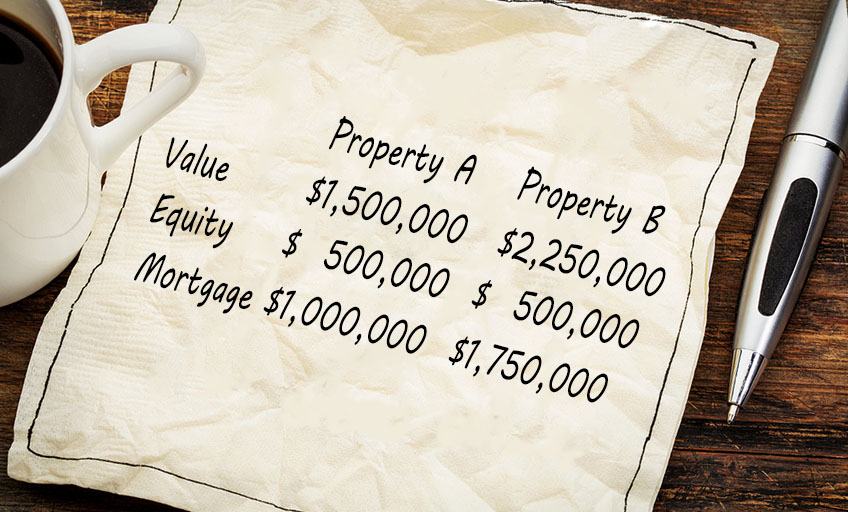

The Napkin test is simply a matter of determining if the Exchangor is trading across or up in value, equity and mortgage. The Exchangor’s current property is “A” and the property to be acquired is “B.”

Here, the Exchangor is trading up in value, across in equity and up in mortgage; therefore, he has no taxable boot.

What is Boot

Boot is “unlike” property received in an Exchange. Cash, personal property, or a reduction in the mortgage owed after an Exchange are all boot and subject to tax. By forecasting the potential for taxable boot, the Exchangor can restructure the transaction before committing to the deal. “Mortgage boot” results when an Exchangor reduces the amount of loan or debt by exchanging. If the loan on the original property was $1,000,000 and the loan on the acquired property is $900,000, there is $100,000 worth of mortgage boot, which may be taxable. An easy way to understand mortgage boot is to use a simple loan as an example. If you lend $100,000 to a friend and only require him to pay back $70,000, he will have received $30,000 of income. He will have to pay tax on this income.

A Simple Rule to Remember

You may offset mortgage boot with cash, but you cannot offset cash boot with additional mortgage. In the above example, the Exchangor can add $100,000 of cash to offset the mortgage boot. However, if the Exchangor has $1,000,000 worth of net equity and trades into a building with only $900,000 of equity, the Exchangor receives $100,000 in cash and that cannot be offset with a larger loan.