#1. When a property is transferred it must be as an Exchange, not a sale.

The absolute essence of an Exchange is that something must be given away (relinquished property) and something must be received (replacement property). Property that is sold, and not Exchanged, does not qualify. A property is disqualified even if the property has been sold inadvertently. Usually, the reason for the unintended sale is based upon the tax principal of “constructive receipt of funds.”

Constructive receipt is when the Exchangor has the right to receive or control funds even though the Exchangor has not yet directly accessed those funds. An Exchangor who receives a check payable to them for their property interest has sold the property, even though they have not cashed the check.

An Exchangor who transfers their property interest to a buyer with sale proceeds deposited directly into a neutral account (such as an escrow account or an account opened by the Exchangor’s attorney) has sold the property and no longer qualifies for an Exchange. It is irrelevant whether the Exchangor has cashed the check or pulled money out of escrow. Constructive receipt of funds occurred when the Exchangor obtained his right to access funds.

The Exchangor may also inadvertently sell their property upon receipt of a significant amount of non-refundable earnest money. The IRS may characterize this large payment as the first of two or more payments for the property. In other words, the non-refundable payment triggered the transfer of the property interest and the Exchangor has constructive receipt of the subsequent payments as they become due and payable.

To help ensure a sale does not occur when the intent was to Exchange, it is recommended you inform both your broker and a 1031 Exchange Facilitator early about your intent to Exchange.

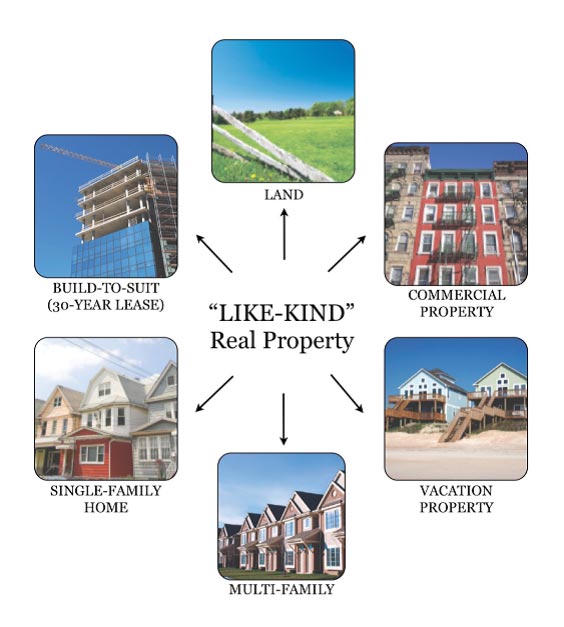

#2. The properties being Exchanged must be of like-kind.

Like-kind refers to the nature and character of the properties. Similar classes of property are called “like-kind.” Like-kind requirements differ depending on the type of property you are selling (real property versus personal property ).

Real Property Like-Kind Requirements

The class for real property (real estate) is very broad. It includes vacant land, office buildings, houses, warehouses, shopping centers and any other form of real estate held for investment purposes. Even leases with more than 30 years remaining are considered investment property and can be traded for other real estate.

Personal Property Like-Kind Requirements

Unlike real property, it becomes more difficult to state when personal property is like-kind to other personal property. Personal property Exchanges are more restrictive because of the various classifications that pertain to personal property. Personal property may be characterized as either depreciable tangible property or intangible property and non-depreciable personal property.

Depreciable tangible personal property

Depreciable tangible personal properties are considered like-kind if they are like-class; that is, Exchanged properties must be in the same class. The classes are established in the tax regulations as General Asset Class and Product Class . If a product may be classified within a General Asset Class, it may not be re-classified into a Product Class.

Intangible and non-depreciable personal properties

Intangible and non-depreciable personal properties are Exchanged for like-kind property (there are no “like-class” guidelines for these types of properties). The nature or character of the rights involved, as well as the nature or character of the underlying property to which the intangible personal property relates, determines whether the property is “like-kind.” Items that fall under intangible and non-depreciable personal properties include some patents, forms of software, copyrights and trademarks.

#3. The Napkin Test must be satisfied.

For an Exchange to be completely tax deferred, the value, equity and mortgage on the replacement property should be equal to or greater than that of the relinquished property. Normal transactional costs can be deducted to determine replacement property value. An investor may Exchange into a replacement property of lower value without invalidating the Exchange, although taxes will be paid on the spread.

It is possible to reduce or totally eliminate debt on the replacement property by adding cash to a purchase. The amount of cash added must offset any reduction in debt.

The Napkin Test is a simple exercise to determine the potential for exposing taxable assets or “boot” in an Exchange by comparing the values of the relinquished and replacement property(ies).

#4. There must be continuity of vesting from the relinquished property to the replacement property.

The party/tax payer giving up the relinquished property must receive the replacement property.